|

|

|

|

|

|

|

|

| LEADERSHIP TEAM & ADVISORY BOARD |

| closely together |

|

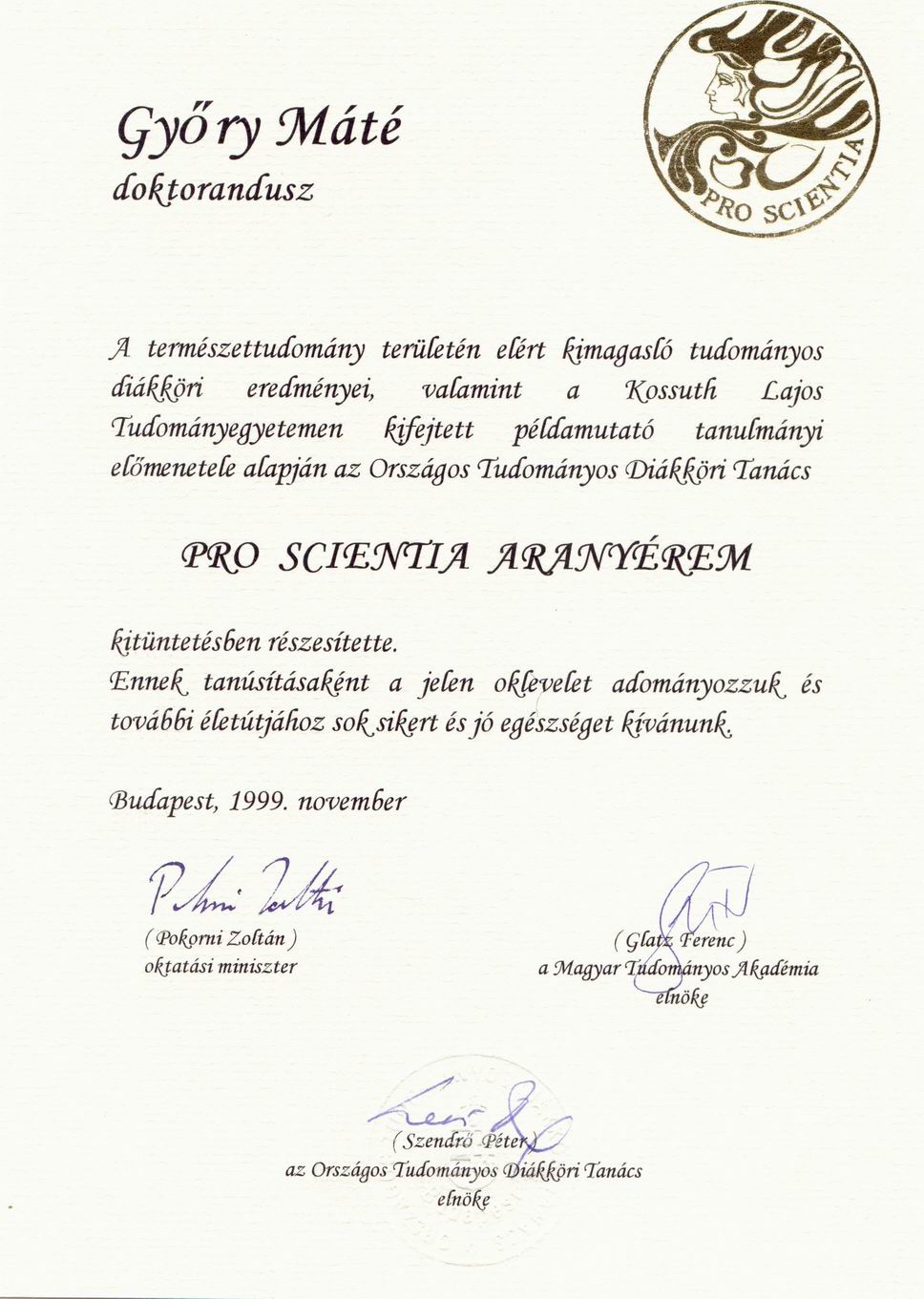

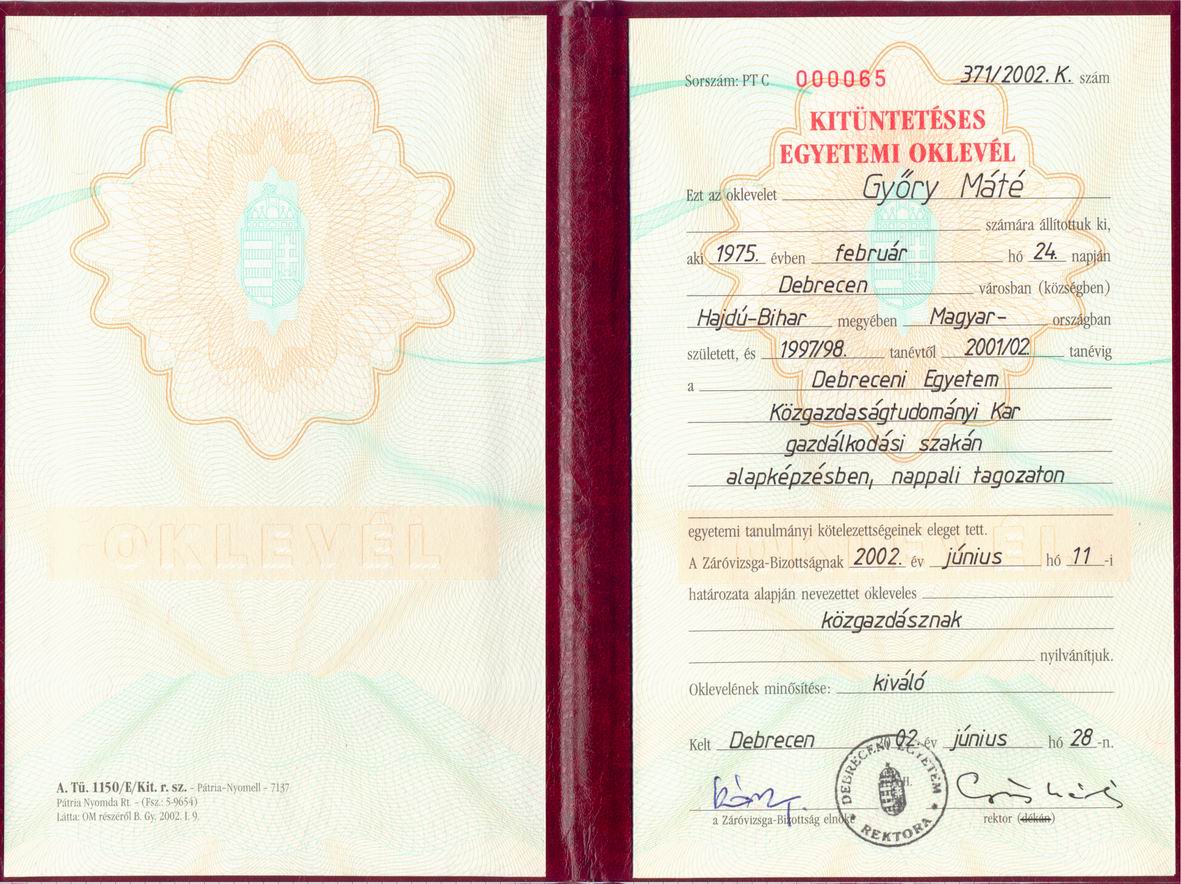

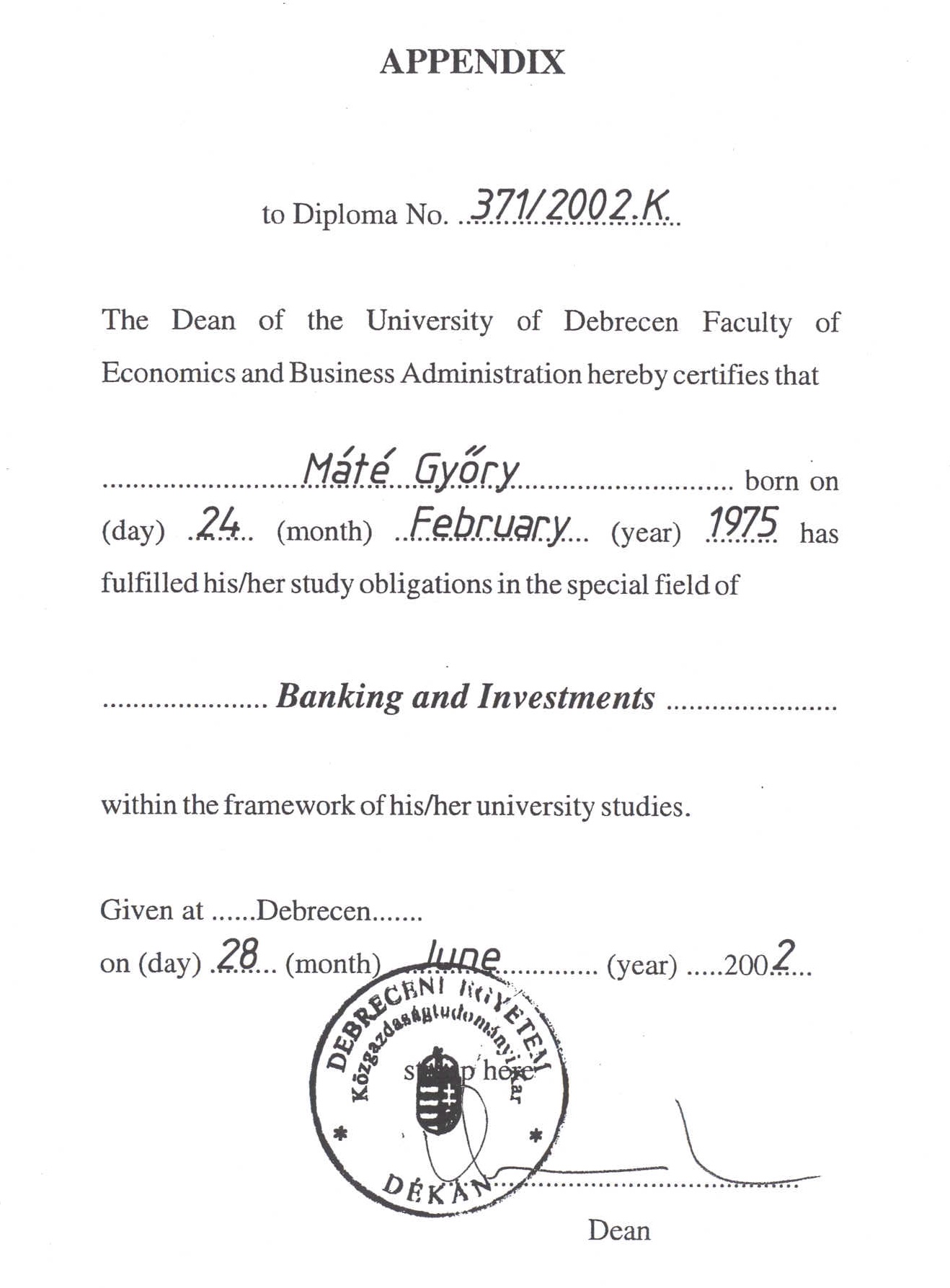

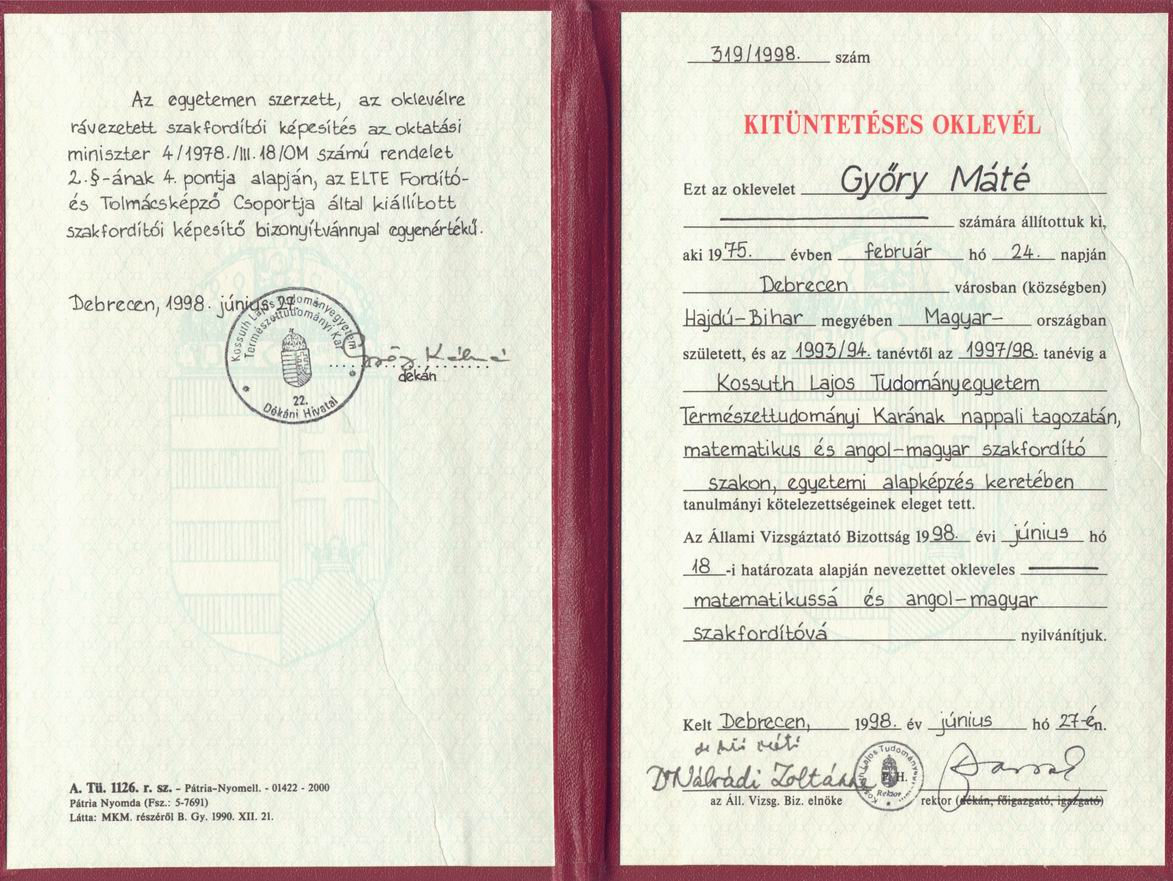

Mathematician, economist (specialised on banking and investment) with a Ph.D. in mathematics. Achieved his two M.Sc. degrees and his Ph.D. degree with distinction. Former university professor and academic researcher. Quantitative analyst with 16 years' experience in investment banks and other analytical firms. Founding member of Morgan Stanley's Mathematical Modelling Centre in 2006. Leads the company since 2016. Read more |

|

Entrepreneur, artist, pianist, flutist, singer. Graduated with distinction. Founded, built and made her own music school in London successful in partnership with her husband. Successfuly managed several projects for distinguished clients. Works for the company since 2016. Read more |

|

Physicist, with a Ph.D in Astronomy. Former academic researcher with a successful decade-long academic career. Quantitative analyst and Commodity and Power Risk specialist with 16 years' experience in the industry. Founding member of Morgan Stanley's Mathematical Modelling Centre in 2006. Read more |

|

Software Engineer and Economist with M.Sc. degrees of Computer Science and Finance. Held various leadership positions, including Global Head of Core Analytics at Morgan Stanley (managed 40 quants globally), Head of Analytics Integration at RBC Capital Markets (30 quants) and Core Analytics at Deutsche Bank. Senior Quantitative Analyst with exceptional software design, code optimization and mathematical skills and 20 years' experience in software development focusing on quantitative, analytical and algorithmic problems. Founding member of the Mathematical Modelling Centre in 2006. Read more |

|

Mathematical modeler and software engineer with an M.Sc. in Informatics and a Ph.D. in Technical Sciences. During his 16 years at Morgan Stanley, worked in New York and Budapest, held various leadership positions, including Budapest Head of Risk Analytics (45 quants), Budapest Head of Global Macro Analytics and Modelling (25 quants), and Head of Global Macro Market Modelling. Has vast experience with developing pricing models for credit and interest rate derivatives and risk management. Founding member of the Mathematical Modelling Centre in 2006. Read more |

|

Senior Software Engineer and Front Office Quantitative Developer, with an M.Sc. of Technical Informatics. Held various positions at J.P. Morgan, Mercuria Energy Trading and more than 10 years at Morgan Stanley. Closely worked together with the mathematicians through various phases of the models’ lifecyle: from the implementation to the deployment to production in the Mathematical Modelling Centre from 2007. Read more |

|

Financial mathematician, with a Ph.D in Financial Econometrics from Tilburg University. Runs VAR Strategies, a retireTech quant startup. Held various senior quantitative analytics leadership positions at global investment banks. Visiting professor of quantitative finance at prestigious universities. Quantitative analyst with 23 years' experience in the industry. As EMEA Head of Fixed Income Research at Morgan Stanley, former manager of Mate Gyory and Andras Szell. Read more |

|

Software engineer with a summa cum laude Ph.D. in Data Science. Author, former university professor and academic researcher. A polyglot data engineer with 15 years' experience at top tier institutions, specializing in high performance computing, big data and cloud solutions. Held various positions at KX and during his more than 13 years at Morgan Stanley. As EMEA Head of Business Metrics at Morgan Stanley's Fixed Income Division, had strong co-operation with FID Sales and Trading and the Mathematical Modelling Centre after 2006. Read more |

| The main source of our talent pool are the many excellent,

skillful quantitative analysts and quantitative developers with whom we worked and whom we managed throughout our careers. We know who is good and in what, who is reliable and co-operative. This gives us an excellent network, a large superb talent pool

and a great advantage. We have experienced experts with deep and up-to-date knowledge in all fields of quantitative analytics, financial mathematical modelling, financial derivatives, risk management, quantitative development, programming, testing, back-testing, documentation. We have a deep understanding of the market of finiancial derivatives and utilise it to our clients' needs. |

| Mathematician, economist (specialised on banking and investment) with a Ph.D. in mathematics. Achieved his two M.Sc. degrees and his Ph.D. degree with distinction. Former university professor and academic researcher. Quantitative analyst with 16 years' experience in investment banks and other analytical firms. Founding member of Morgan Stanley's Mathematical Modelling Centre in 2006. Leads the company since 2016. |

|

|

|

|

|

|

|

|

|

Entrepreneur, artist, pianist, flutist, singer. Graduated with distinction. Founded, built and made her own music school in London successful in partnership with her husband. Successfuly managed several projects for distinguished clients.

Works for the company since 2016. |

|

|

|

|

|

Physicist, with a Ph.D in Astronomy. Former academic researcher with a successful decade-long academic career. Quantitative analyst and Commodity and Power Risk specialist with 16 years' experience in the industry.

Founding member of Morgan Stanley's Mathematical Modelling Centre in 2006. |

|

|

|

|

|

Software Engineer and Economist with M.Sc. degrees of Computer Science and Finance.

Held various leadership positions at investment banks, including Global Head of Core Analytics at Morgan Stanley (managed 40 quants globally), Head of Analytics Integration at Royal Bank of Canada Capital Markets (managed 30 quants) and Core Analytics at Deutsche Bank.

Senior Quantitative Analyst with exceptional software design, code optimization and mathematical skills and 20 years' software development experience focusing on quantitative, analytical and algorithmic problems.

Founding member of the Mathematical Modelling Centre in 2006. |

|

|

|

|

| Mathematical modeler and software engineer with an M.Sc. in Informatics and a Ph.D. in Technical Sciences. During his 16 years at Morgan Stanley, worked in New York and Budapest, and held various leadership positions, including Budapest Head of Risk Analytics (managing 45 quants), Budapest Head of Global Macro Analytics and Modelling (managing 25 quants), and Head of Global Macro Market Modelling. Has vast experience with developing pricing models for credit and interest rate derivatives and risk management. Founding member of the Mathematical Modelling Centre in 2006. |

|

|

|

|

| Senior Software Engineer and Front Office Quantitative Developer, with an M.Sc. of Technical Informatics. Held various positions at J.P. Morgan, Mercuria Energy Trading and more than 10 years at Morgan Stanley. Made invaluable work on putting the mathematical models into production in the Mathematical Modelling Centre after 2007. |

|

|

|

|

|

Financial mathematician, with a Ph.D in Financial Econometrics from Tilburg University. Runs VAR Strategies, a retireTech quant startup.

Held various senior quantitative analytics leadership positions at global investment banks. Visiting professor of quantitative finance at prestigious universities.

Quantitative analyst with 23 years' experience in the industry.

As EMEA Head of Fixed Income Research at Morgan Stanley, former manager of Mate Gyory and Andras Szell. |

|

|

|

|

|

Software engineer with a summa cum laude Ph.D. in Data Science. Author, former university professor and academic researcher.

A polyglot data engineer with 15 years' experience at top tier institutions, specializing in high performance computing, big data and cloud solutions.

Held various positions at KX and during his more than 13 years at Morgan Stanley. As EMEA Head of Business Metrics at Morgan Stanley's Fixed Income Division,

had strong co-operation with FID Sales and Trading and the Mathematical Modelling Centre after 2006. |

|

|

|

|